Whole Life vs Indexed Universal Life Insurance: Which is Best for You?

It’s like the iconic ‘Get a Mac’ Mac vs PC advertising campaign from the mid-2000s: two products, two personalities, each with its own appeal. Whole Life and Indexed Universal Life Insurance are similar – distinct choices catering to different financial and life goals.

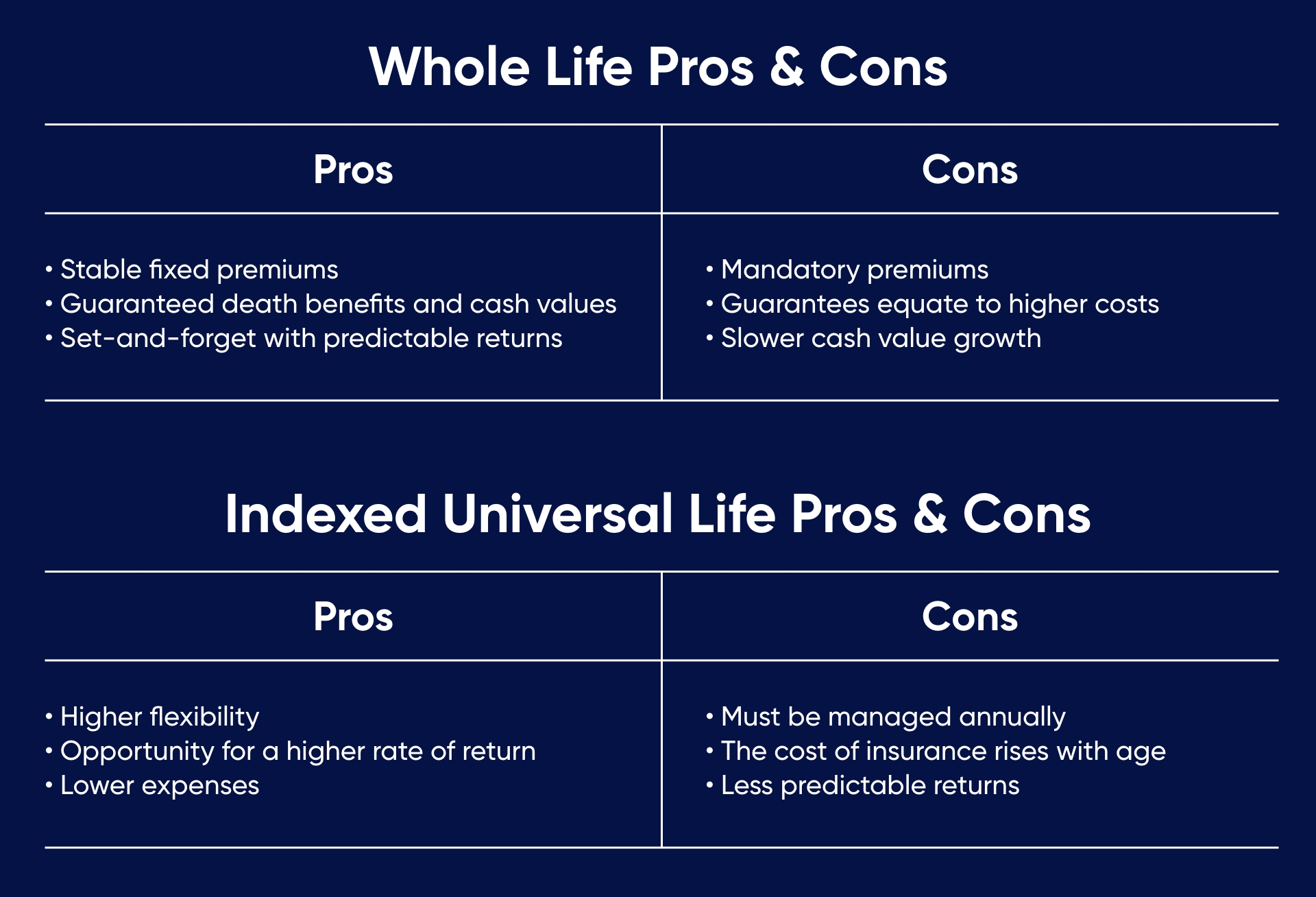

- Both options offer tax-free cash value

- Whole Life is more rigid and comes with a higher cost

- Indexed Universal Life offers flexibility with lower fees

- Whole Life is predictable and offers guaranteed cash value growth vs Indexed Universal Life, which has more risk, but also a greater growth opportunity

An analogy, because why not?

Let’s imagine the two life insurance policies are competing travel companies: Whole Life Leisure Holidays and Indexed Universal Life Adventures.

The Whole Life Leisure Holidays brochure features a grainy 1970s design of a couple in matching resort wear enjoying the all-inclusive Cancun vacation they’ve booked every holiday for the past 30 years: the same buffet, same playlist, same guests, same reliable experience.

In contrast, Indexed Universal Life Adventures promises a wide-eyed couple wearing sensible hiking shoes endless possibilities on the road less traveled. With expert guides providing comfort, the journey blends part-planned with the freedom to explore new paths, allowing for magic moments.

Which would you choose?

What are Indexed Universal Life and Whole Life insurance policies?

Both policy types are a form of permanent cash value life insurance. This means you can access the funds while you’re alive, and they can be tax-free. The ‘cash value’ represents the excess premiums and earnings on investments from the policy’s early years to create reserves above the policy’s internal expenses.

Whole Life vs Indexed Universal Life

WHOLE LIFE

Whole Life does what it says on the box: providing your premiums are paid, you’re covered for your lifetime. Overall, Whole Life is steady but more rigid. It’s generally designed at either a 10-pay, 15-pay or 20-pay strategy, or where the policyholder is paying for the entirety of life. The cash value of Whole Life is equal to the death benefit. So, some might ask, what good is a life insurance policy if the death benefit you’ll receive is equal to the cash value that you could take out of the policy? With no leverage on the death benefit, it’s like just having a bank account. What is appealing to some is Whole Life’s guaranteed death benefit and fixed premiums. But with that in mind, its predictability and security attract much higher fees.

INDEXED UNIVERSAL LIFE

An Indexed Universal Life policy offers more flexibility. You can structure it according to your strategy and objectives, accumulating cash value with the option to draw on that or allow the policy to grow. Missed a payment? No problem, make up for it at a later date. Prefer to pay over a short period, such as we do for the Stream Protection Plan? No problem. Indexed Universal Life is designed for agility and growth opportunities. Its model features a death benefit but includes a component that’s tied to a particular stock market index used to help grow cash value, unlike Whole Life, which hinges on the insurance carrier’s performance. Lower fees are also a significant factor. If borrowing rates are at eight percent for Whole Life, in comparison, you’d expect approximately three percent for Indexed Universal Life.

In summary

Whole Life appeals to those whose primary object is security and who are willing to pay for that guarantee. But suppose you're looking to hyper fund your retirement and allow agility with a more modern stress-tested model of tax-free premium financed life insurance. In that case, Indexed Universal Life might be for you.

Want to know more?

Connect with our team of experts to assess what’s best for you and design a policy that sets you up for life.